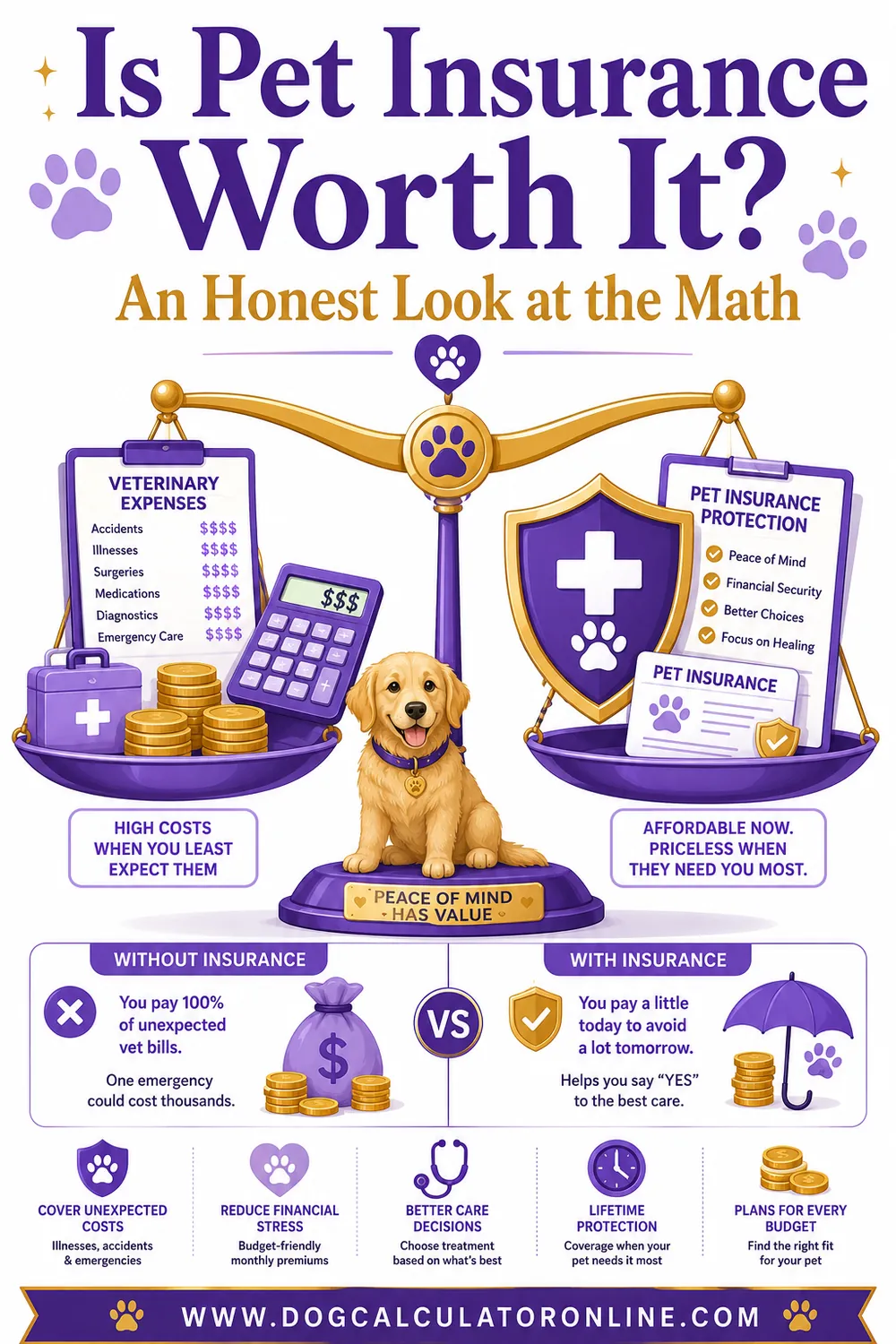

Is Pet Insurance Worth It? An Honest Look at the Math

Pet insurance is worth it if a surprise $3,000–$6,000 vet bill would force you into debt or into an impossible decision about your dog's care — and it's often not worth it if you have a healthy emergency fund and the discipline to keep it funded. Typical accident-and-illness coverage for dogs runs about $40–$70 per month depending on breed, age, and state. This guide walks through the honest math on both sides, with no carrier pitches — and our free dog cost calculator helps you see where insurance fits in your total budget.

The Short Answer

Pet insurance is a financial product, not a moral one — so the question is purely mathematical and personal. It comes down to three things:

- Could you absorb a $5,000 bill tomorrow without hardship? If yes, self-insuring is viable. If no, insurance is doing real work for you.

- Is your dog high-risk? Some breeds carry well-documented predispositions (joint problems in large breeds, breathing issues in flat-faced breeds) that make claims more likely.

- Will you actually save the money instead? The self-insurance plan only works if the account genuinely gets funded every month.

Roughly speaking, an insured owner pays a predictable $500–$850 a year and may never "profit" from it. An uninsured owner saves that money — until the year they don't. Neither choice is wrong. Being unprepared in both directions is wrong.

What Pet Insurance Actually Covers

Most dog policies are accident and illness plans. Here's the typical shape:

- Covered: injuries (broken bones, swallowed objects, bite wounds), illnesses (infections, cancer, diabetes), diagnostics (X-rays, bloodwork, MRIs), surgeries, hospitalization, prescription meds — usually including hereditary conditions if they weren't already showing symptoms when you enrolled.

- Not covered: pre-existing conditions (anything diagnosed or symptomatic before coverage started), routine and preventive care (exams, vaccines, flea/heartworm prevention) unless you buy a wellness add-on, and typically things like grooming, breeding costs, and cosmetic procedures.

You also choose three dials that set both your premium and your protection:

| Dial | Common options | Effect |

|---|---|---|

| Reimbursement rate | 70% / 80% / 90% | Higher rate = higher premium |

| Annual deductible | $250 / $500 / $1,000 | Higher deductible = lower premium |

| Annual payout limit | $5,000 / $10,000 / unlimited | Higher limit = higher premium |

One structural thing to understand: with most plans you pay the vet up front and get reimbursed after filing a claim. You still need enough cash or credit to cover the bill for a few days to a few weeks.

The Real Math: Insurance vs. Self-Insuring

Let's run honest numbers for a medium-sized dog over a 12-year life.

The insured path. At an average of $55/month (premiums rise as dogs age — starting lower for puppies, higher for seniors), you'll pay roughly $7,000–$9,000 in lifetime premiums, plus deductibles and your co-pay share when claims happen.

The self-insured path. Put the same $55/month into a savings account and you'll accumulate about $660 a year. After five years you'd have roughly $3,300 plus interest — enough for one major event.

Now the two scenarios that decide everything:

- The lucky dog: minor issues only, lifetime vet surprises under $3,000. Self-insuring wins clearly — you keep the difference, several thousand dollars.

- The unlucky dog: a swallowed toy at age 2 ($3,500) before the fund has grown, a torn cruciate at age 6 ($5,000), cancer at age 11 ($8,000). Insurance wins dramatically — and the age-2 event is the killer for self-insurers, because it lands before the fund exists.

That early-years gap is the strongest genuine argument for insurance: savings accounts start at zero, coverage doesn't. The strongest genuine argument against: most dogs are closer to lucky than unlucky, which is precisely how insurers stay in business.

To make it concrete, here's a worked claim on a typical plan (80% reimbursement, $500 annual deductible): your dog tears a cruciate ligament and the surgery plus rehab totals $4,500. You pay the vet $4,500 up front. The insurer subtracts your $500 deductible, then reimburses 80% of the remaining $4,000 — a check for $3,200. Your true out-of-pocket: $1,300, plus the year's premiums. Painful, but a very different event than eating the full $4,500 — and that difference is the entire product. Run the same arithmetic on a $900 bill, though, and reimbursement shrinks to $320; insurance earns its keep on the big events, not the small ones.

When Pet Insurance Is Clearly Worth It

Insurance earns its premium most reliably when:

- You couldn't cover a $3,000–$5,000 bill without debt or agonizing choices. This is the core case. Insurance means the treatment decision gets made on medicine, not on money — what vets sometimes call avoiding "economic euthanasia."

- You have a high-risk breed. French Bulldogs, English Bulldogs, Great Danes, German Shepherds, Bernese Mountain Dogs and others carry well-known predispositions that make large claims statistically likelier.

- Your dog is young and healthy right now. Enrolling early locks in coverage before anything becomes "pre-existing." Waiting until problems appear defeats the entire mechanism.

- You live in a high-cost vet market. Big-city specialty and ER prices can run far above national ranges, making the same policy protect against bigger numbers.

- You know yourself. If the savings account would quietly become vacation money, the forced discipline of a premium has real value.

When Self-Insuring Makes More Sense

Skipping insurance is a legitimate strategy when:

- You already have $5,000+ in accessible emergency savings and replenishing it wouldn't wreck you.

- You'll genuinely automate the transfer — same amount, every month, untouchable except for the dog.

- Your dog is older with pre-existing conditions. Once major conditions are excluded, premiums (which rise steeply with age) can buy surprisingly little coverage. The money may protect you better in a savings account.

- You have multiple pets. Premiums multiply per pet, but one shared emergency fund can back all of them, since they're unlikely to all have disasters the same year.

If you go this route, treat it like a bill: automatic transfer, separate account, funded on day one — ideally seeded with a lump sum so you're never exposed in the early years.

How to Decide in 10 Minutes

- Check your emergency fund. Under $2,000 accessible → lean insurance. Over $5,000 → self-insuring is on the table.

- Look up your breed's common conditions. Two or more expensive predispositions → lean insurance.

- Consider your dog's age. Under ~5 and healthy → good time to insure. Senior with existing conditions → run the numbers skeptically; the answer may be savings.

- Get 2–3 real quotes for your actual dog (breed, age, ZIP). Premiums vary widely — our guide to how much pet insurance costs for a dog breaks down every factor.

- Whichever you choose, start now. The worst plan is the one you're still deciding on when the sock gets swallowed.

Fine Print That Changes the Math

If you do go the insurance route, four contract details matter more than the marketing page:

- Waiting periods. Coverage doesn't start the day you pay. Accidents typically have a short wait (a few days to two weeks), illnesses around 14 days, and orthopedic conditions like cruciate tears often 6 months or more. Anything that appears during the wait counts as pre-existing.

- Bilateral condition clauses. If your dog tears one cruciate ligament before enrolling (or during a waiting period), many policies exclude the other knee too — and second-knee tears are common. This single clause decides whether insurance makes sense for a lot of large-breed owners.

- Exam fees and taxes. Some policies reimburse the vet's exam fee as part of a sick visit; others quietly don't, leaving you $75–$150 out of pocket per visit before the "covered" part begins.

- Per-condition vs. annual deductibles. An annual deductible resets once a year no matter how many problems arise; a per-condition deductible applies separately to each new diagnosis. For a dog with multiple issues in one year, the difference is hundreds of dollars.

None of these make insurance a bad product — they make skimming the policy a bad plan. Ten minutes with the sample contract answers all four.

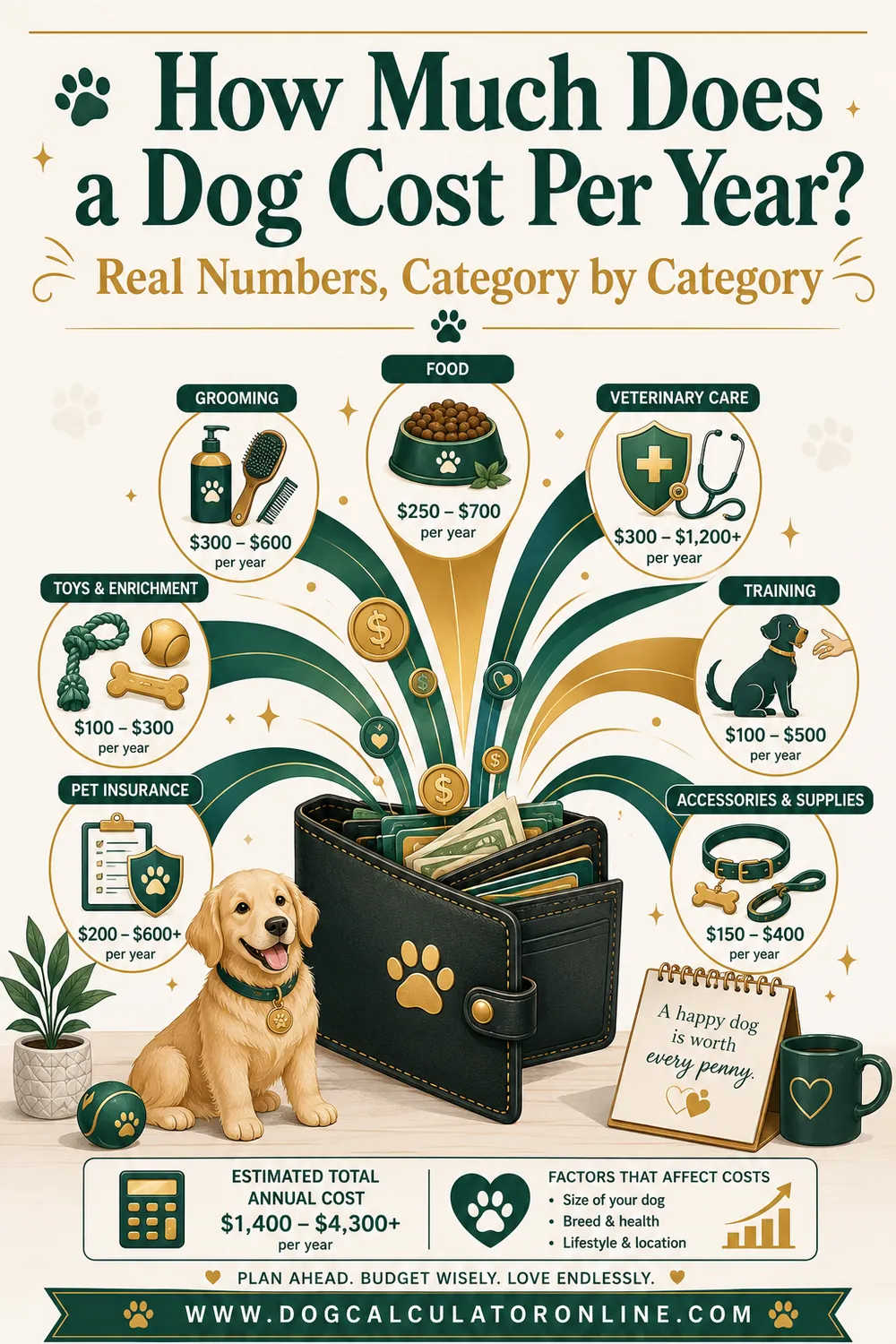

Where does this fit in the bigger picture? Insurance-or-savings is one of the three big lines in your annual dog budget — see the full breakdown in how much a dog costs per year, or run your own numbers with the free dog cost calculator.

FAQ

Is pet insurance worth it for a healthy young dog?

That's actually when it's most worth considering — premiums are at their lowest and nothing is pre-existing yet. The counterargument is that young healthy dogs claim less. The tiebreaker is your savings: thin cushion, insure; thick cushion, either works.

What does pet insurance cost for a dog?

Accident-and-illness plans commonly run $40–$70 per month in the US, with the real range stretching from about $25 to well over $100 depending on breed, age, location, and the deductible/reimbursement options you pick.

Does pet insurance cover pre-existing conditions?

Essentially no — conditions that were diagnosed or symptomatic before enrollment (or during the waiting period) are excluded. Some insurers distinguish curable past conditions (like a healed ear infection) and may cover recurrences after a symptom-free period, but chronic conditions stay excluded.

Is it better to put money in savings instead of pet insurance?

It can be — if you fund it consistently, seed it early, and accept the risk of a big bill arriving before the fund matures. Insurance buys certainty; savings buys flexibility and keeps the surplus in the lucky scenario.

When is it too late to get pet insurance?

Some insurers have senior age limits for new enrollment, and premiums climb steeply with age — but the practical "too late" is after a major condition is diagnosed, because it will be excluded from any new policy.

Should I get the wellness add-on too?

Wellness plans mostly pre-pay predictable costs (vaccines, exams) with a fee on top. They're a budgeting convenience, not risk protection. Do the arithmetic: if the add-on costs more than the routine care it reimburses, skip it.

The Bottom Line

Insurance is worth it when a big bill would hurt more than the premium does — and that's a fact about your finances, not about dogs in general. Decide once, set it up, and move on to the fun parts of dog ownership. For the full financial picture, from food portions to lifetime costs, the free dog calculators have you covered.