How Much Is Pet Insurance for a Dog? Costs by Age, Breed, and State

Pet insurance for a dog typically costs $40–$70 per month for accident-and-illness coverage in the US — roughly $480 to $840 a year — though real quotes range from about $25 for a young small mixed-breed in a low-cost state to well over $100 for a senior bulldog in a big city. Your price is set by five factors: breed, age, location, and the deductible and reimbursement levels you choose. This guide shows how each one moves the number, so the quotes you get actually make sense — and the free dog cost calculator shows how a premium fits into your whole yearly budget.

Average Pet Insurance Cost for Dogs

For the standard product — an accident-and-illness plan with common settings (80% reimbursement, $250–$500 deductible, mid-range annual limit) — most US dog owners see quotes in the $40–$70 per month band. Accident-only plans, which skip illness coverage entirely, are far cheaper at roughly $15–$25 per month, but they won't help with the cancers, infections, and chronic conditions that generate most senior-dog bills.

| Plan type | Typical monthly cost | What it covers |

|---|---|---|

| Accident-only | $15–$25 | Injuries: broken bones, swallowed objects, wounds |

| Accident + illness | $40–$70 | Injuries plus sickness, cancer, hereditary conditions |

| Accident + illness + wellness | $60–$95 | Adds routine care reimbursement (exams, vaccines) |

Treat these as orientation ranges, not promises — the same dog can get quotes 2× apart from different insurers, which is exactly why understanding the factors below (and comparing several real quotes) matters.

The 5 Factors That Set Your Premium

1. Breed

Breed is often the biggest single factor, because insurers price on decades of claims data. Breeds with well-documented health predispositions cost more to insure:

- Priciest tier: flat-faced breeds (French Bulldog, English Bulldog, Pug — breathing and skin issues), giant breeds (Great Dane, Mastiff — shorter lifespans, joint problems, bloat risk), and Rottweilers.

- Mid tier: popular large breeds like Labs, Goldens, and German Shepherds (hips, elbows, cruciate ligaments), plus Cavaliers (heart) and Dachshunds (backs).

- Cheapest tier: small and medium mixed-breed dogs, which benefit from genetic diversity and smaller bodies (lower drug doses and surgery costs).

A mixed-breed dog of the same size as a purebred is usually meaningfully cheaper to insure.

2. Age

Premiums climb steadily — and eventually steeply — with age, because older dogs simply claim more:

- Puppy to age 2: the cheapest window. This is also when enrolling locks in coverage before anything becomes a pre-existing condition.

- Ages 3–6: modest annual increases.

- Ages 7+: increases accelerate; by age 10, premiums are commonly 2–3× the puppy-age price for the same dog and plan. Some insurers also cap new enrollments for seniors.

Important nuance: your premium generally rises at renewal even without claims, both because your dog is older and because vet costs inflate. Budget for the premium you'll pay at age 8, not just the one you're quoted today. (Curious what your dog's age really means biologically? Our dog age chart shows the size-adjusted conversion.)

3. Location

Insurance is priced against local vet costs, so your ZIP code matters. Owners in major metros — New York, San Francisco, Seattle, Boston — often pay 30–50% more than owners in lower-cost states for identical coverage, simply because a cruciate surgery that costs $3,200 in a small city might be $5,500 downtown. Rural and Southern states generally sit at the low end.

4. Deductible

The annual deductible — what you pay out of pocket before reimbursement starts — is your biggest controllable lever:

- $100–$250 deductible: highest premium, coverage kicks in fastest

- $500 deductible: the popular middle ground

- $750–$1,000 deductible: substantially cheaper premium; you're only covered for genuinely large events

Moving from a $250 to a $500 deductible typically cuts a noticeable slice off the monthly price, and it aligns with the smartest use of insurance anyway: protection against disasters, not reimbursement for every small visit.

5. Reimbursement Rate and Annual Limit

Two more dials, same logic:

- Reimbursement: 70%, 80%, or 90% of covered costs after the deductible. 90% plans cost the most; 70% plans leave you with a bigger share of every bill.

- Annual limit: $5,000, $10,000, or unlimited payout ceilings. The jump from $5,000 to $10,000 usually costs little and protects against exactly the scenarios insurance exists for — a single $8,000 event blows straight through a $5,000 cap.

A sensible default for most owners: 80% reimbursement, $500 deductible, $10,000+ or unlimited annual limit. Adjust from there based on your cash cushion.

Example Profiles: What Real Quotes Tend to Look Like

Every insurer weighs things differently, but these composite profiles show how the factors stack:

| Dog | Typical monthly range |

|---|---|

| 1-year-old small mixed breed, Ohio | $25–$45 |

| 4-year-old Beagle, Texas | $35–$60 |

| 3-year-old Labrador, California | $55–$90 |

| 2-year-old French Bulldog, New York | $70–$120 |

| 9-year-old Golden Retriever, Florida | $90–$150 |

Notice the pattern: small + mixed + young + cheap state stacks every discount, while flat-faced or senior + big city stacks every surcharge.

How to Lower Your Pet Insurance Cost

Without gutting the coverage that makes insurance useful:

- Enroll young. Locking in before any diagnosis is the single most valuable move — it keeps conditions coverable and starts you at the bottom of the age curve.

- Raise the deductible to $500 or more, and keep that amount in savings instead.

- Skip the wellness add-on unless the math clearly favors it — it mostly pre-pays predictable costs with a fee attached.

- Ask about discounts: multi-pet (often 5–10%), annual-pay, military, and employer benefit programs are common.

- Compare at least three quotes for your exact dog. Spreads of $20–$40/month between insurers for the same coverage are routine.

- Consider accident-only for a tight budget — partial protection genuinely beats none, especially for young dogs whose biggest risks are swallowed objects and injuries.

One caution: switching insurers later restarts pre-existing condition exclusions. Anything diagnosed under the old policy becomes pre-existing under the new one, so cheap-hopping between carriers can quietly erase your most valuable coverage.

How to Compare Quotes Apples-to-Apples

Two quotes for "$45/month" can be wildly different products. When you compare, lock these settings identical across every quote before judging the price:

- Same reimbursement rate (say, 80%) — a cheap 70% plan isn't cheaper, it just shifts cost to claim time.

- Same deductible ($500 is a sensible comparison point) and same deductible type — annual, not per-condition.

- Same annual limit — compare $10,000 to $10,000, or unlimited to unlimited.

- Then check what's quietly different: whether exam fees are covered, how long the orthopedic waiting period runs, whether hereditary conditions are included (they usually are on major plans, but verify for your breed), and whether the insurer caps payouts per condition.

Also worth asking: how the insurer handles renewals. Premiums rise everywhere, but some carriers raise rates by age curve only, while others adjust based on local claims trends more aggressively. A plan that's $5 cheaper today and climbs faster is the worse deal by year six.

Finally, quote your actual dog honestly — age, breed or best-guess mix, and ZIP. Fudging a mixed breed as "unknown" or shaving a year off the age can void claims later, which is the most expensive discount there is.

Does filing claims raise my premium? With most US pet insurers, no — unlike auto insurance, individual claims history generally doesn't set your personal renewal price. Premiums rise with your dog's age, local veterinary cost inflation, and the insurer's overall claims experience in your area, whether or not you personally filed anything. That's worth knowing for two reasons: don't skip legitimate claims out of fear of a rate hike, and don't expect a claim-free year to earn you a discount either. The renewal letter will go up modestly most years regardless; that's the age curve doing its thing, not a penalty.

Premiums in Context: Your Total Dog Budget

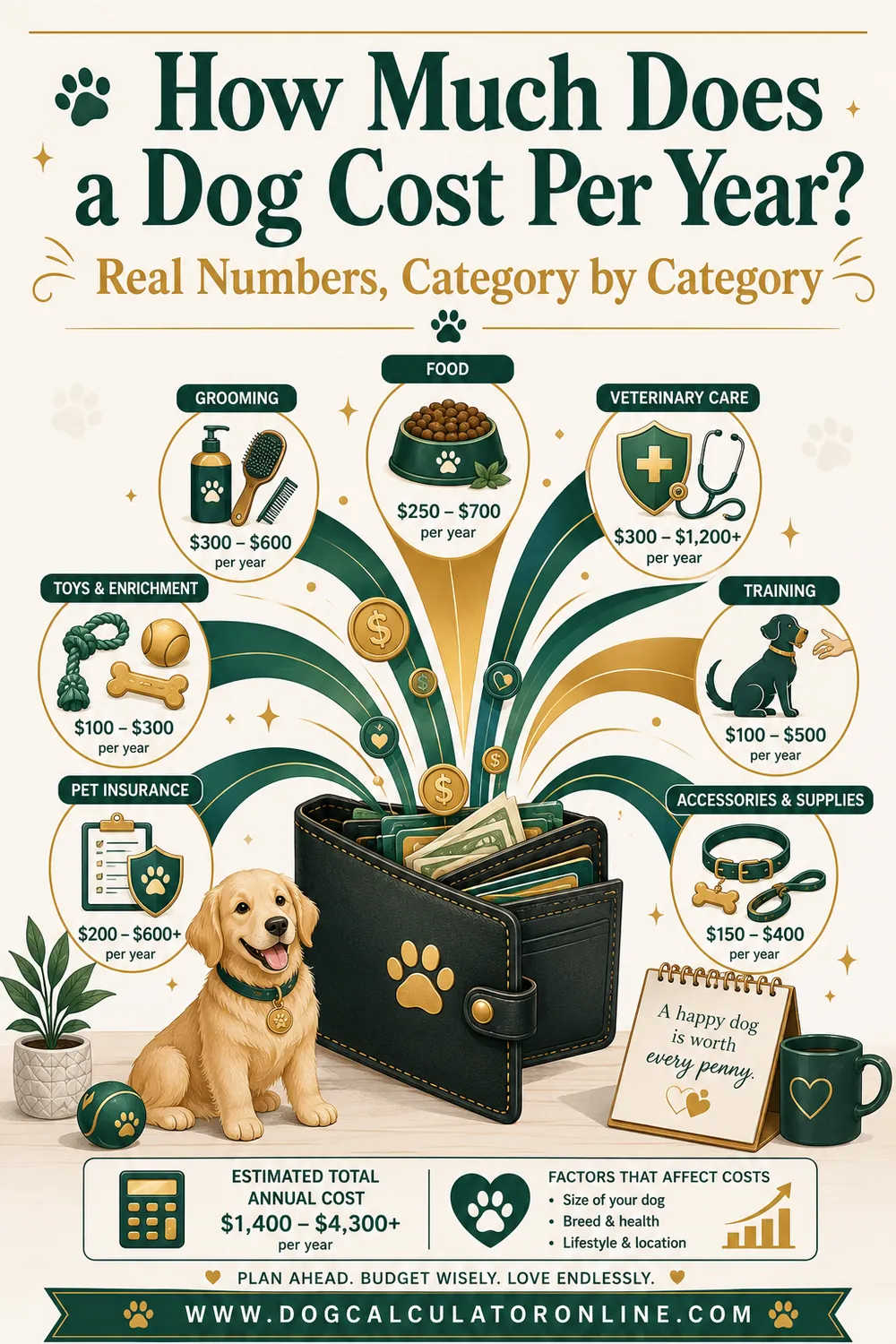

A $55/month premium is about $660 a year — sitting alongside food ($250–$900), routine vet care ($300–$800), and everything else in a typical $1,500–$4,000 annual cost of ownership. For most insured owners, the premium lands as the second or third largest line in the dog budget, which is exactly why it deserves the ten minutes of comparison shopping most people never give it. Whether that premium is the right spend for you is a separate question from what it costs — we walk through that decision, including the self-insurance alternative, in is pet insurance worth it, and the full budget picture in how much a dog costs per year.

FAQ

How much is pet insurance for a dog per month?

Most US dog owners pay $40–$70 per month for accident-and-illness coverage. Small young mixed breeds can come in around $25–$35; flat-faced breeds, seniors, and big-city dogs can exceed $100.

Why is my quote so much higher than average?

Almost always one of four things: a breed with documented health risks, an older dog, a high-cost metro area, or rich plan settings (low deductible, 90% reimbursement, unlimited payout). Adjust the settings and re-quote to see which is driving it.

Does pet insurance get more expensive as my dog ages?

Yes — expect increases at most renewals, accelerating in the senior years. By age 10 a premium is commonly two to three times its puppy-age level. Factor the senior-years price into your decision, not just today's quote.

Is cheaper accident-only coverage worth having?

For a tight budget, yes — at $15–$25/month it covers the sudden traumatic stuff (swallowed objects, broken bones) that hits young dogs hardest. Just know it pays nothing toward illnesses, which dominate costs later in life.

What deductible should I choose?

If you have a few hundred dollars of cushion, a $500 deductible usually hits the sweet spot: meaningfully cheaper than $250, while keeping the catastrophic protection intact. Pick the highest deductible you could comfortably pay tomorrow.

Do all vets accept pet insurance?

Effectively yes, because most plans reimburse you rather than paying the vet — you can use any licensed vet, ER, or specialist. You pay the bill, file the claim, and receive the covered portion back.

Get a Number You Can Trust

Now you can read any quote intelligently: breed, age, ZIP, deductible, reimbursement — that's the whole formula. Get two or three real quotes for your dog, pick sensible dials, and slot the result into your budget with the free dog cost calculator to see the complete picture of what your dog costs per year.